Market at all time high, but where are the FPIs?

A remarkable statistic

12/4/20232 min read

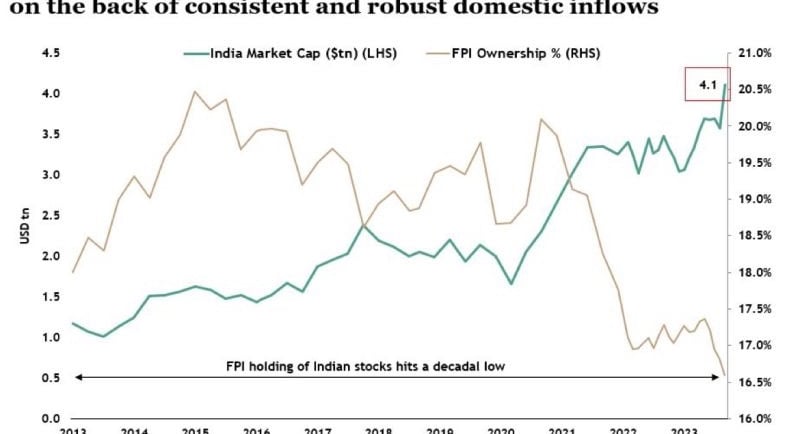

Friday December 1, 2023 was a strong day for Indian equity markets as the Nifty closed at a record 20,200. There is however an aspect of this weeks’ rise that has nothing to do with FPI buying or a general increase of interest in the India story for global investors. It is remarkable to see that FPI holding in Indian equities is at a decadal low. The above chart shows the lack of correlation to the markets over the last few years. This is quite counter intuitive if you rely on the older paradigm that Indian equities rise when FPI’s buy.

Of course the data needs to be analysed a little more in detail to come to any concrete conclusion but the lower holding is even more dramatic when compared with the value of the market today compared to 2015. 20% of the then market cap compared to just over 16% of the total market cap today is owned by FPIs. This actually represents an even bigger sell down than the actual numbers indicate in value terms.

FPI’s clearly have booked hefty gains over this period and are looking for bargains elsewhere. This could be one conclusion to arrive at.

Does this hold any indicators to valuation in India?

India has traditionally been an expensive market and the premium is unlikely to reduce. The main reason would possibly be the lower floating stock available for large investors. Typically promoters of Indian listed companies own the largest chunk of the ownership and as a result even 20% of FPI ownership is significant given the lower floating stock. While promoters are not diluting their stake the domestic mutual funds and domestic investors are steadily making gains in the ownership ladder. This is a reason to remain pretty optimistic about the sustenance of the premium in coming years. The demand and supply for any commodity determines the price at any time and considering that the investing public in India is just getting significantly invested in domestic equities there is more room to grow. Hence it will be too early to throw in the towel and to conclude that India equities are expensive on P/E ratio alone as there may be other factors involved. is however an aspect of this weeks’ rise that has nothing to do with FPI buying or a general increase of interest in the India story for global investors.